Understanding Accrual Accounting for Small Businesses: Accrual And Inventory For Small Business

Accrual and inventory for small business – Accrual accounting, unlike cash accounting, recognizes revenue when earned and expenses when incurred, regardless of when cash changes hands. This provides a more accurate picture of a business’s financial health over time. This section will detail the differences between cash and accrual accounting, explore the advantages and disadvantages of accrual accounting for small businesses, provide examples of common accrual accounting entries, and present a sample chart of accounts.

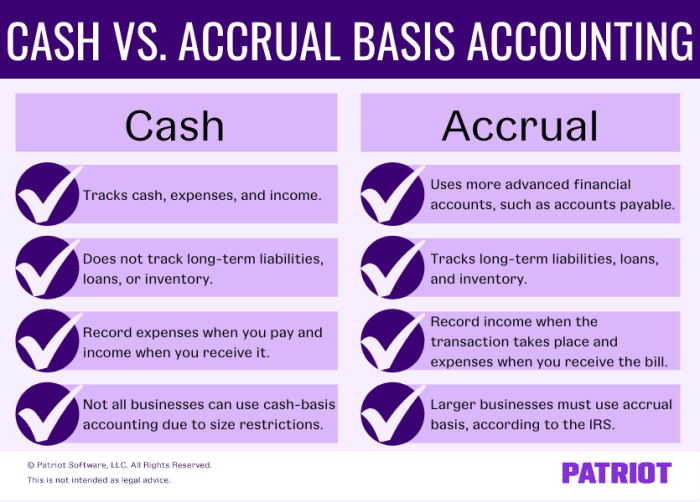

Cash vs. Accrual Accounting

Cash accounting records transactions when cash is received or paid. Accrual accounting records revenue when it’s earned and expenses when they’re incurred, regardless of when cash is exchanged. For example, if a business provides services in December but receives payment in January, cash accounting would record the revenue in January, while accrual accounting would record it in December.

Advantages and Disadvantages of Accrual Accounting for Small Businesses

Accrual accounting offers a more accurate reflection of a business’s financial performance. However, it requires more complex record-keeping.

- Advantages: More accurate financial statements, better understanding of profitability and cash flow, improved creditworthiness.

- Disadvantages: More complex record-keeping, requires more accounting expertise, potentially more time-consuming.

Examples of Common Accrual Accounting Entries

Here are some common accrual accounting entries relevant to small businesses:

- Accounts Receivable: Recording revenue earned but not yet paid. For example, a sale of $100 on credit would be recorded as a debit to Accounts Receivable and a credit to Sales Revenue.

- Accounts Payable: Recording expenses incurred but not yet paid. For example, purchasing $50 worth of supplies on credit would be recorded as a debit to Supplies and a credit to Accounts Payable.

Sample Chart of Accounts for a Small Retail Business

Source: patriotsoftware.com

| Account Name | Account Type | Account Number |

|---|---|---|

| Cash | Asset | 101 |

| Accounts Receivable | Asset | 102 |

| Inventory | Asset | 103 |

| Accounts Payable | Liability | 201 |

| Sales Revenue | Revenue | 401 |

| Cost of Goods Sold | Expense | 501 |

| Operating Expenses | Expense | 502 |

Inventory Management for Small Businesses

Effective inventory management is crucial for small businesses to maintain profitability and avoid stockouts or overstocking. This section will cover different inventory valuation methods, compare periodic and perpetual inventory systems, highlight the importance of accurate inventory tracking, and illustrate a simple inventory management system using a spreadsheet.

Inventory Valuation Methods

Different methods exist for valuing inventory, each impacting the cost of goods sold and ultimately, profitability. The three most common methods are:

- FIFO (First-In, First-Out): Assumes the oldest inventory is sold first.

- LIFO (Last-In, First-Out): Assumes the newest inventory is sold first. (Note: LIFO is less commonly used for financial reporting purposes under IFRS).

- Weighted-Average Cost: Calculates the average cost of all inventory items.

The choice of method can significantly affect the reported cost of goods sold and net income, especially during periods of fluctuating prices.

Periodic vs. Perpetual Inventory Systems, Accrual and inventory for small business

These systems differ in how inventory is tracked. A periodic system updates inventory levels only at the end of a period, while a perpetual system updates inventory continuously with each transaction.

Example: Periodic System: A small bookstore counts its inventory at the end of each month. If the beginning inventory was 100 books and 200 books were purchased during the month, with 150 books sold, the ending inventory would be calculated as 100 + 200 – 150 = 150 books.

Example: Perpetual System: The same bookstore uses a point-of-sale system that tracks each book sold and purchased in real-time. Inventory levels are constantly updated.

Importance of Accurate Inventory Tracking

Accurate inventory tracking is vital for several reasons:

- Accurate Financial Reporting: Ensures correct cost of goods sold and profit calculations.

- Efficient Inventory Management: Prevents stockouts and overstocking, optimizing cash flow.

- Improved Decision-Making: Provides data for informed decisions regarding purchasing, pricing, and sales strategies.

Simple Inventory Management Spreadsheet

| Item Name | Quantity | Cost per Item | Total Value |

|---|---|---|---|

| T-shirt | 50 | $10 | $500 |

| Jeans | 30 | $25 | $750 |

| Sweater | 20 | $15 | $300 |

Accrual Accounting and Inventory Interaction

Accrual accounting and inventory management are intrinsically linked. Accurate inventory tracking is essential for correct financial reporting under accrual accounting. This section will explore the key interactions between these two aspects, provide examples of inventory-related transactions under accrual accounting, and demonstrate how inventory errors can affect financial statements.

Key Interactions

The primary interaction lies in the calculation of the cost of goods sold (COGS). COGS is an expense that directly impacts a business’s profitability. Accurate inventory tracking is crucial to accurately determine COGS under accrual accounting.

Examples of Inventory-Related Transactions

Examples include:

- Purchase of Inventory: Debit Inventory, Credit Accounts Payable (if on credit) or Cash (if paid in cash).

- Sale of Inventory: Debit Accounts Receivable (or Cash), Credit Sales Revenue. Simultaneously, debit Cost of Goods Sold and credit Inventory.

Impact of Inventory Errors

Inventory errors directly impact the accuracy of the cost of goods sold and consequently, net income. Overstated inventory leads to understated COGS and overstated net income, while understated inventory has the opposite effect.

Step-by-Step Process for Recording Inventory Purchases and Sales

Source: debitoor.com

- Purchase: Record the purchase of inventory by debiting the Inventory account and crediting either Cash or Accounts Payable.

- Sale: Record the sale of inventory by debiting either Cash or Accounts Receivable and crediting Sales Revenue. Simultaneously, debit Cost of Goods Sold and credit Inventory for the cost of the goods sold.

- Inventory Adjustment (if needed): At the end of the period, adjust the Inventory account to reflect any discrepancies between physical inventory count and recorded inventory levels.

Practical Applications and Challenges

Implementing and maintaining accurate accrual accounting and inventory systems can present challenges for small businesses. This section will discuss common accounting software solutions, common challenges, the importance of regular inventory counts, and provide a checklist for ensuring accuracy.

Accrual accounting and accurate inventory management are crucial for small businesses to maintain healthy finances. Understanding how inventory impacts your bottom line is key, and a significant aspect of this is recognizing that a change in business inventories is, as explained in this helpful resource, a change in business inventories is , a direct reflection of sales and production.

Therefore, effectively tracking both accruals and inventory allows for better financial planning and informed business decisions.

Accounting Software Solutions

Several accounting software solutions cater to small businesses’ needs, offering features for both accrual accounting and inventory management. Examples include Xero, QuickBooks, and Zoho Books. These software packages automate many tasks, reducing the manual effort required for accurate record-keeping.

Challenges in Implementation and Maintenance

Source: etsystatic.com

Small businesses often face challenges such as:

- Lack of Accounting Expertise: Requires training or outsourcing accounting functions.

- Time Constraints: Maintaining accurate records can be time-consuming.

- Cost of Software and Training: Implementing accounting software involves initial costs and ongoing maintenance expenses.

Importance of Regular Inventory Counts and Reconciliation

Regular physical inventory counts are essential to identify discrepancies between recorded and actual inventory levels. Reconciling these differences helps maintain accuracy and prevent financial statement errors.

Checklist for Accurate Accrual Accounting and Inventory Management

- Implement an appropriate accounting software solution.

- Regularly record all inventory transactions.

- Conduct periodic physical inventory counts.

- Reconcile inventory records with physical counts.

- Ensure proper training for staff involved in inventory management.

- Review financial statements regularly to identify potential discrepancies.

Visualizing Inventory and Financial Data

Visual representations of inventory levels and cost of goods sold can provide valuable insights into a business’s performance. This section will describe how to visualize this data using line and bar charts.

Visualizing Inventory Levels Over Time (Line Graph)

A line graph is ideal for showing inventory levels over time. The x-axis would represent time (e.g., months), and the y-axis would represent inventory quantity. Each data point would represent the inventory level at a specific point in time. A line connecting these points would illustrate the trend of inventory levels over the period.

Visualizing Cost of Goods Sold as a Percentage of Revenue (Bar Chart)

A bar chart effectively displays the cost of goods sold as a percentage of revenue for different periods. The x-axis would represent the time periods (e.g., quarters), and the y-axis would represent the percentage. Each bar would represent the percentage of revenue that was attributed to the cost of goods sold during that period. This allows for easy comparison of COGS as a proportion of revenue across different periods.

FAQ Explained

What is the best inventory valuation method for my small business?

The optimal method depends on your specific industry and inventory characteristics. FIFO (First-In, First-Out) is common for perishable goods, while LIFO (Last-In, First-Out) can be advantageous in times of inflation. Weighted-average cost provides a simpler approach.

How often should I perform inventory counts?

Regular inventory counts, ideally monthly or quarterly, are crucial for maintaining accuracy. The frequency depends on your inventory turnover rate and the risk of loss or shrinkage.

What accounting software is recommended for small businesses using accrual accounting?

Many options exist, including QuickBooks, Xero, and Zoho Books. The best choice depends on your specific needs and budget. Consider features like inventory tracking, reporting capabilities, and ease of use.

Can I switch from cash accounting to accrual accounting?

Yes, but it requires careful planning and potentially professional assistance. The transition involves adjusting your accounting records to reflect the accrual method, which can be complex.