Introduction to the No Inventory Method

Accounting for no inventory method for small business – The no inventory method, also known as the direct costing method, is a simplified accounting approach particularly suitable for small businesses that don’t hold significant inventory. This method directly records sales revenue and expenses related to those sales, bypassing the complexities of tracking and valuing inventory.

Concept of the No Inventory Method, Accounting for no inventory method for small business

Unlike traditional inventory accounting methods (FIFO, LIFO, weighted average), the no inventory method eliminates the need for detailed inventory tracking. Sales revenue is recorded directly, and the cost of goods sold (COGS) is calculated based on the direct expenses associated with fulfilling those sales. This approach significantly streamlines the accounting process, making it ideal for businesses with minimal or no inventory holding.

Appropriate Circumstances for the No Inventory Method

This method is most appropriate for small businesses operating under specific conditions. These include businesses with minimal or no physical inventory, those offering services rather than products, or businesses that utilize a drop-shipping model where goods are shipped directly from the supplier to the customer. Examples include businesses providing consulting services, freelance work, or digital product sales.

Examples of Businesses Using the No Inventory Method

Several small businesses effectively utilize this method. For instance, a freelance graphic designer doesn’t hold physical inventory; their income is directly tied to service provision. Similarly, a small online business selling digital downloads like e-books or software avoids inventory management entirely. A consultant offering business advisory services also operates without significant inventory.

Advantages of the No Inventory Method for Small Businesses: Accounting For No Inventory Method For Small Business

The no inventory method offers several advantages for small businesses, primarily simplification and cost reduction in accounting.

Simplified Accounting Processes

This method significantly reduces the complexity of accounting. Tracking and valuing inventory is a time-consuming task, and eliminating this step streamlines the entire accounting process, allowing businesses to focus on core operations.

Reduced Administrative Burden

The reduced complexity translates to a lower administrative burden. Businesses save time and resources that would otherwise be spent on inventory management tasks like stock counts, valuation adjustments, and managing discrepancies.

Cost Savings Associated with Inventory Management

Eliminating inventory tracking reduces costs associated with inventory management software, storage, and potential losses due to spoilage or obsolescence. This translates to direct cost savings for the business.

Comparison of Inventory Accounting Methods

| Method | Complexity | Cost | Suitability for Small Businesses |

|---|---|---|---|

| No Inventory | Low | Low | High (for suitable businesses) |

| FIFO | High | Medium-High | Medium (for businesses with significant inventory) |

| LIFO | High | Medium-High | Medium (for businesses with significant inventory and specific tax advantages) |

Disadvantages and Limitations of the No Inventory Method

While advantageous, the no inventory method also has limitations, particularly for businesses with fluctuating sales or those requiring precise cost of goods sold calculations.

Potential Drawbacks for Businesses with Fluctuating Sales

Source: thestartupboy.com

For businesses with highly variable sales, this method might not accurately reflect the true cost of goods sold, leading to potential inaccuracies in profit calculations. The simplicity comes at the cost of detailed cost tracking.

Implications for Financial Reporting Accuracy

The simplified nature of the method can compromise the accuracy of financial reporting, especially when compared to more detailed inventory accounting methods. This is particularly relevant for businesses seeking precise financial statements for external stakeholders like investors or lenders.

Limitations in Providing Accurate Cost of Goods Sold Calculations

Without detailed inventory tracking, calculating the cost of goods sold can be less precise. This can affect the accuracy of profit margins and other key financial metrics.

Challenges in Managing Potential Discrepancies

The lack of granular inventory control can make it challenging to identify and resolve discrepancies between actual sales and recorded revenue. This can potentially lead to errors in financial reporting.

Accounting Procedures under the No Inventory Method

The accounting procedures under this method are simplified, focusing on direct recording of sales and related expenses.

Recording Sales Revenue Directly

Sales revenue is recorded directly as it is generated, without the intermediate step of recording inventory movements.

Tracking Expenses Related to Goods Sold

Expenses directly related to the sale, such as direct materials, direct labor, and direct shipping costs, are tracked and recorded as part of the cost of goods sold.

Calculating Gross Profit Without Detailed Inventory Valuation

Gross profit is calculated by subtracting the direct costs of goods sold from the sales revenue. This eliminates the need for complex inventory valuation calculations.

Step-by-Step Guide for Implementation

- Identify all direct costs associated with each sale.

- Record sales revenue immediately upon completion.

- Record the associated direct costs.

- Calculate gross profit by subtracting total direct costs from total sales revenue.

- Regularly reconcile sales and expense records.

Tax Implications of the No Inventory Method

The no inventory method can impact tax filings, primarily by affecting the calculation of cost of goods sold and ultimately, taxable income.

Impact on Tax Filings

The simplified calculation of cost of goods sold directly affects the reported net income, which in turn influences tax liability. This simplification can either reduce or increase tax liability depending on the specific circumstances.

Specific Tax Forms and Reporting Requirements

While the basic tax forms remain the same, the method of calculating cost of goods sold needs to be clearly documented and justifiable. Consult with a tax professional to ensure compliance.

Examples of How the Method Might Affect Tax Liability

In a scenario with consistently high sales and low direct costs, the no inventory method might result in a higher tax liability compared to a traditional method that includes inventory valuation adjustments. Conversely, with fluctuating sales and high direct costs, the tax implications might be less predictable.

Scenario Illustrating Tax Implications

Consider a small business selling handmade crafts. Using the no inventory method, direct material costs are deducted directly, potentially resulting in a lower taxable income compared to a FIFO method where inventory valuation might increase taxable income in certain periods. The impact depends heavily on the timing of sales and purchases.

Software and Tools for Implementing the No Inventory Method

Several accounting software solutions support the no inventory method, offering features tailored to businesses operating under this model.

Suitable Accounting Software

Many cloud-based accounting software options readily accommodate this method. Features like simple expense tracking and direct sales recording are crucial.

Required Features and Functionalities

Essential features include streamlined expense tracking, simple sales recording, and reporting capabilities that accurately reflect the direct costing approach. Integration with other business tools is also beneficial.

Comparison of Software Options

Software options vary in pricing and features. Some offer basic functionalities at a lower cost, while others provide more advanced features at a higher price point. Choosing the right software depends on the specific needs of the business.

Essential Features for Accounting Software

- Simple sales entry

- Direct expense tracking

- Automated gross profit calculation

- Customizable reports

- Cloud-based accessibility

Case Studies: Small Businesses Using the No Inventory Method

Several small businesses have successfully implemented the no inventory method, demonstrating its effectiveness in specific contexts.

Examples of Successful Implementations

A freelance writer, for instance, directly records their income from projects and expenses related to those projects, simplifying their accounting. A small online course provider also benefits from this method, as their product is digital and requires no physical inventory.

Experiences and Reasons for Adoption

Businesses often adopt this method for its simplicity and cost-effectiveness. The reduced administrative burden allows them to focus on core business activities rather than complex inventory management.

Best Practices and Lessons Learned

Accurate tracking of direct expenses is crucial. Regular reconciliation of sales and expenses is also vital to maintain accuracy and avoid potential discrepancies.

Challenges Faced and How They Were Overcome

Challenges might include initially adapting to a different accounting approach. Proper training and clear documentation can help overcome this hurdle. Also, businesses need to ensure that all relevant expenses are accurately categorized and recorded.

Understanding accounting for the no inventory method is crucial for small businesses; accurate record-keeping is essential for profitability. However, effective management goes beyond simple accounting; consider the insights offered by the 7-eleven business leadership inventory test to assess your operational efficiency. This test can help identify areas for improvement, ultimately strengthening your financial management, even when employing a no-inventory accounting method.

Comparison with Other Inventory Accounting Methods

The no inventory method differs significantly from traditional methods like FIFO and LIFO in its approach to inventory valuation and cost of goods sold calculation.

Key Differences in Calculations and Reporting

Source: opentextbc.ca

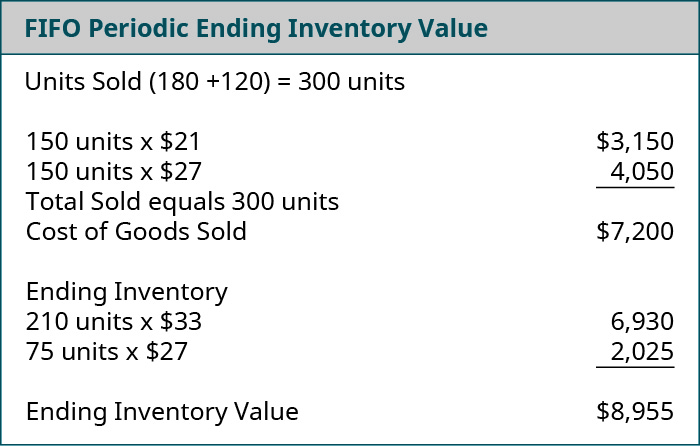

FIFO and LIFO involve detailed tracking of inventory movements and valuation, leading to more complex calculations and reporting. The no inventory method simplifies these processes by eliminating the need for inventory tracking.

Scenarios Where Each Method is Most Suitable

Source: cashflowinventory.com

FIFO and LIFO are best suited for businesses with substantial physical inventory, while the no inventory method is ideal for businesses with minimal or no inventory.

Advantages and Disadvantages of Each Method

| Method | Advantages | Disadvantages | Best Suited For |

|---|---|---|---|

| No Inventory | Simple, low cost, reduced administrative burden | Less accurate COGS, unsuitable for businesses with significant inventory | Service-based businesses, businesses with minimal inventory, drop-shipping businesses |

| FIFO | Relatively simple, generally accepted accounting principle | Complex for large inventories, can lead to higher taxes in inflationary periods | Businesses with significant inventory, those needing GAAP compliance |

| LIFO | Can lead to lower taxes in inflationary periods | Complex, not allowed under IFRS, can lead to lower net income | Businesses with significant inventory, those seeking tax advantages in inflationary periods (where allowed) |

Essential Questionnaire

What if my business occasionally holds a small amount of inventory?

The no-inventory method is best suited for businesses with minimal or no inventory. Occasional inventory might necessitate adjustments or a hybrid approach. Consult with an accountant to determine the best strategy.

Can I use the no-inventory method for tax purposes regardless of my accounting method?

The method used for accounting purposes generally aligns with tax reporting. However, specific tax regulations vary by jurisdiction. Always consult a tax professional for accurate guidance.

How does the no-inventory method affect my business valuation?

The absence of inventory significantly impacts valuation. Consult a business valuation expert to understand the implications for your specific circumstances.

What if I make a mistake using the no-inventory method?

Errors can be corrected through standard accounting adjustments. Maintaining meticulous records is crucial for accurate financial reporting and minimizing potential issues.