Understanding the Retail Method of Inventory Costing: A Business Using The Retail Method Of Inventory Costing Determines

A business using the retail method of inventory costing determines – The retail method is a valuable inventory costing technique frequently used by retailers to estimate the cost of goods sold (COGS) and ending inventory. It simplifies inventory valuation by using the relationship between the cost and retail price of goods. This method is particularly useful for businesses with a large number of items and frequent price changes, where tracking each item’s cost individually would be impractical.

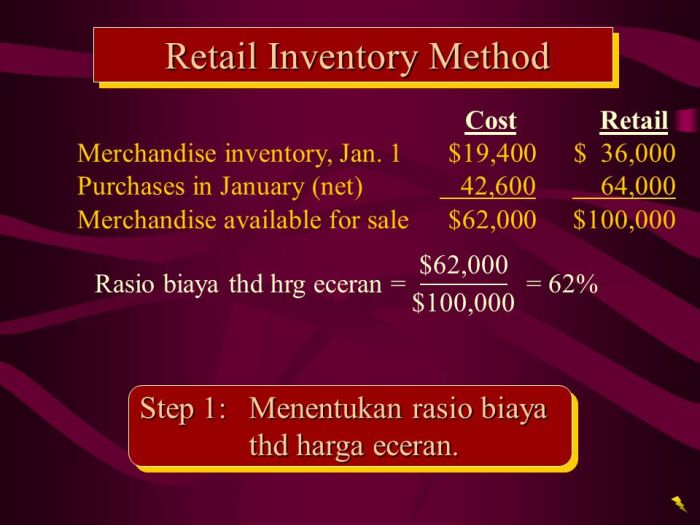

The Retail Method and its Principles

Source: slideplayer.info

The retail method operates on the principle that a consistent relationship exists between the cost and the retail price of inventory. This relationship, expressed as a cost-to-retail percentage, is used to estimate the cost of goods available for sale and the cost of ending inventory. The underlying assumption is that the markup percentage remains relatively stable throughout the accounting period.

This method is generally acceptable under Generally Accepted Accounting Principles (GAAP) for interim reporting and in certain situations for year-end reporting.

The Retail Method Formula

The core formula for the retail method involves calculating the cost-to-retail percentage and applying it to the ending inventory at retail price. The formula is as follows:

Cost of Goods Available for Sale at Cost / Cost of Goods Available for Sale at Retail = Cost-to-Retail Percentage

Cost of Goods Available for Sale is calculated as Beginning Inventory + Purchases. This percentage is then applied to the ending inventory at retail to estimate the cost of ending inventory.

Businesses Using the Retail Method

The retail method is commonly employed by businesses with high inventory turnover and a large number of similar items, such as:

- Department stores

- Grocery stores

- Clothing retailers

- Pharmacies

- Discount stores

Retail Method vs. Other Inventory Costing Methods

The retail method differs from other inventory costing methods like FIFO (First-In, First-Out), LIFO (Last-In, First-Out), and weighted-average in its approach. FIFO and LIFO track the cost of each item, while the weighted-average method calculates a weighted average cost. The retail method, in contrast, uses a cost-to-retail percentage to estimate costs, making it simpler for businesses with high inventory volume.

The retail method provides a quicker estimation than the other methods, but it’s less precise as it relies on estimations rather than tracking individual item costs.

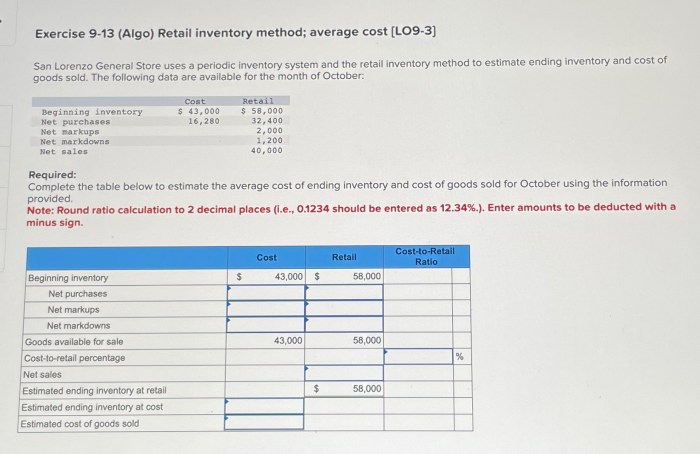

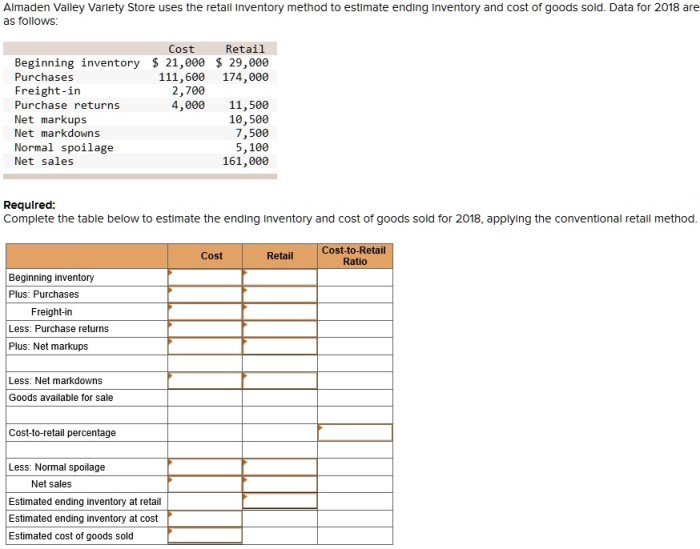

Calculating Cost of Goods Sold (COGS) using the Retail Method

Calculating COGS using the retail method involves a series of steps that utilize the cost-to-retail percentage. Accuracy in each step is crucial for a reliable COGS figure.

Step-by-Step COGS Calculation

The process typically involves these steps: 1. Determine the cost of goods available for sale at cost and retail. 2. Calculate the cost-to-retail percentage. 3.

Determine the ending inventory at retail. 4. Apply the cost-to-retail percentage to the ending inventory at retail to estimate the cost of ending inventory. 5. Calculate the COGS by subtracting the estimated cost of ending inventory from the cost of goods available for sale.

Example Calculation

Let’s illustrate with an example:

| Description | Beginning Inventory | Purchases | Ending Inventory |

|---|---|---|---|

| Cost | $10,000 | $30,000 | ? |

| Retail | $15,000 | $45,000 | $12,000 |

1. Cost of Goods Available for Sale (Cost): $10,000 + $30,000 = $40,000

2. Cost of Goods Available for Sale (Retail): $15,000 + $45,000 = $60,000

3. Cost-to-Retail Percentage: $40,000 / $60,000 = 66.67%

4. Estimated Cost of Ending Inventory: $12,000

– 0.6667 = $8,000

5. Cost of Goods Sold (COGS): $40,000 – $8,000 = $32,000

Impact of Markups and Markdowns

Markups and markdowns significantly affect the cost-to-retail percentage. Markups increase the retail value without changing the cost, leading to a lower cost-to-retail percentage. Markdowns, conversely, reduce the retail value, potentially increasing the cost-to-retail percentage. These adjustments need to be considered when calculating the cost-to-retail percentage to ensure accuracy.

Avoiding Calculation Errors

Common errors include incorrect calculation of the cost-to-retail percentage, inaccurate recording of beginning and ending inventory, and failure to account for markups and markdowns. Careful data entry, regular inventory checks, and a thorough understanding of the formula are crucial to avoid these errors.

Applying the Retail Method to Different Scenarios

Source: cheggcdn.com

Seasonal Inventory Fluctuations

A clothing retailer might experience high inventory levels during peak seasons (e.g., winter for coats) and low levels during off-seasons. The retail method can accurately reflect these fluctuations by calculating a cost-to-retail percentage for each season, accounting for seasonal markdowns and sales.

Inventory Theft or Damage

Source: numerade.com

If a significant portion of inventory is lost due to theft or damage, the retail method can adjust for this loss. By accurately assessing the retail value of the lost inventory and applying the cost-to-retail percentage, the business can estimate the cost of the loss and adjust its COGS and ending inventory accordingly.

Comparative Analysis: Retail Method vs. FIFO, A business using the retail method of inventory costing determines

Let’s consider a bookstore with the following data: Beginning inventory (cost) $5,000, Beginning inventory (retail) $10,000, Purchases (cost) $15,000, Purchases (retail) $30,000, Ending inventory (retail) $8,000. Using the retail method, COGS is calculated as $22,000. Using FIFO, assuming a specific cost flow, COGS might be $20,000. The difference arises because the retail method uses an average cost-to-retail percentage, while FIFO tracks the cost of specific items.

- Retail Method COGS: $22,000 – Uses average cost, simpler calculation.

- FIFO COGS: $20,000 – Tracks specific item costs, more accurate but complex.

- Reason for Variation: The difference reflects the inherent differences in the methods. FIFO tracks actual costs, while the retail method provides an estimate.

Limitations and Advantages of the Retail Method

Advantages of the Retail Method

The retail method offers several advantages, including its simplicity and ease of use, especially for businesses with numerous items. It requires less detailed record-keeping compared to FIFO or LIFO, making it cost-effective. It’s also useful for interim reporting when precise inventory costing is not required.

Limitations and Drawbacks

The primary limitation is its reliance on estimations. The accuracy of the results depends heavily on the stability of the cost-to-retail percentage. Significant markups or markdowns can distort the accuracy of the calculations. It is also less precise than other methods for determining the exact cost of goods sold.

Situations Where the Retail Method is Inappropriate

The retail method might be inappropriate for businesses with a highly variable cost-to-retail percentage, businesses selling unique or high-value items, or businesses requiring precise inventory costing for financial reporting.

Impact of Inaccurate Data

Inaccurate data, such as incorrect recording of beginning inventory, purchases, or ending inventory, will directly impact the accuracy of the cost-to-retail percentage and subsequently the COGS and ending inventory estimations. Regular inventory checks and accurate data entry are vital for the method’s reliability.

Illustrative Example: A Retail Business

Let’s consider “Trendy Threads,” a fictional clothing boutique. They carry a wide range of women’s apparel, from casual wear to formal dresses. Their inventory includes numerous items with varying prices and frequent sales and markdowns. They use a consistent markup policy but adjust prices based on seasonal demand and promotional offers.

Trendy Threads uses a perpetual inventory system, updating inventory records daily. They conduct regular physical inventory counts to reconcile their records and account for shrinkage due to theft or damage. Their pricing strategy is based on a standard markup percentage, adjusted for seasonal demand and promotional activities.

For a given quarter, let’s assume: Beginning inventory (cost) $20,000, Beginning inventory (retail) $40,000, Purchases (cost) $60,000, Purchases (retail) $120,000, Markdowns $5,000, Net Sales $100,000, Ending Inventory (Retail) $35,000. Using the retail method, Trendy Threads can estimate their COGS and ending inventory for the quarter, considering markdowns.

Assumptions: The consistent markup policy is a key assumption. Accurate record-keeping and regular inventory checks are also crucial. The impact of markdowns is factored into the calculation, which is crucial for accuracy.

Essential Questionnaire

What are some common reasons for discrepancies when using the retail method?

Discrepancies can arise from inaccurate initial cost data, inconsistent application of markups and markdowns, shrinkage (theft or damage), or errors in recording sales and purchases.

Can the retail method be used for businesses with highly diverse inventory?

No, the retail method is most effective for businesses with a large number of similar items. Highly diverse inventories require more granular tracking methods.

How does the retail method handle returns?

Returns are generally accounted for by adjusting both the cost and retail values of inventory, ensuring the calculation reflects the actual inventory on hand.

Is the retail method acceptable for tax purposes?

Generally yes, but adherence to generally accepted accounting principles (GAAP) or International Financial Reporting Standards (IFRS) is crucial for accurate and compliant reporting. Specific requirements may vary by jurisdiction.