Understanding Business Inventory on the Balance Sheet: A Business Inventory Is What On Its Balance Sheet

A business inventory is what on its balance sheet – A business’s inventory is a crucial component of its financial health, directly impacting profitability and liquidity. Understanding how inventory is defined, valued, and reported on the balance sheet is essential for accurate financial analysis and effective business management. This article provides a comprehensive overview of business inventory and its implications for financial reporting.

Definition of Business Inventory, A business inventory is what on its balance sheet

In accounting terms, business inventory represents the goods a company holds for the purpose of sale in the ordinary course of business. This includes raw materials, work-in-progress (WIP), and finished goods. The value of inventory directly affects a company’s assets, cost of goods sold, and ultimately, its profitability.

Types of Inventory:

- Raw Materials: These are the basic inputs used in the production process. Examples include wood for furniture manufacturing, cotton for textile production, or silicon for semiconductor manufacturing.

- Work-in-Progress (WIP): This represents partially completed goods that are still undergoing the production process. For instance, a partially assembled car on an automotive assembly line or a partially finished garment in a clothing factory.

- Finished Goods: These are completed products ready for sale to customers. This could be anything from a finished car to a ready-to-wear garment or a packaged food item.

Inventory Valuation Methods: Several methods exist for valuing inventory on the balance sheet, each impacting the cost of goods sold and net income. These include:

- First-In, First-Out (FIFO): This method assumes that the oldest inventory items are sold first. This generally leads to a higher net income during periods of inflation.

- Last-In, First-Out (LIFO): This method assumes that the newest inventory items are sold first. This often results in a lower net income during periods of inflation and lower tax liability.

- Weighted-Average Cost: This method calculates the average cost of all inventory items and uses this average to value the goods sold. It provides a smoother representation of inventory costs compared to FIFO and LIFO.

Inventory’s Placement on the Balance Sheet

Inventory is reported in the current assets section of the balance sheet. Current assets are assets expected to be converted into cash within one year or the operating cycle, whichever is longer.

Relationship with Current Assets: Inventory is a significant component of current assets, along with cash, accounts receivable, and short-term investments. The total current assets provide a snapshot of a company’s short-term liquidity and ability to meet its immediate obligations.

Reason for Current Asset Classification: Inventory is considered a current asset because it’s intended to be sold within the normal operating cycle of the business, generating cash in the near future.

A business inventory represents a significant asset, appearing on the balance sheet as a current asset. Understanding how to properly account for inventory is crucial, and for small businesses, navigating regulations like those outlined in the 1.263a-1f inventory small business guidelines is essential. Accurate inventory valuation directly impacts the company’s financial health as reflected on its balance sheet.

Impact of Inventory on Financial Statements

The chosen inventory valuation method significantly affects the cost of goods sold (COGS) and net income. Different methods can lead to variations in reported profits, impacting financial ratios and investor perception.

Overstating vs. Understating Inventory: Overstating inventory inflates assets and net income, while understating inventory has the opposite effect. Both scenarios misrepresent the financial health of the company and can have serious consequences.

Impact on Statement of Cash Flows: Changes in inventory levels directly affect the statement of cash flows. An increase in inventory represents a cash outflow (as cash is used to purchase more inventory), while a decrease represents a cash inflow (as inventory is sold, generating cash).

| Scenario | Effect on Cash Flow from Operating Activities | Effect on Investing Activities | Overall Cash Flow Impact |

|---|---|---|---|

| Increase in Inventory | Decreases (due to higher COGS) | N/A | Decreases |

| Decrease in Inventory | Increases (due to lower COGS) | N/A | Increases |

| No Change in Inventory | No significant direct impact | N/A | No significant direct impact |

| Significant Inventory Write-down | Increases (due to reduced COGS) | N/A | Increases |

Inventory Management and its Reflection on the Balance Sheet

Source: accountingcapital.com

Effective inventory management is crucial for minimizing waste, maximizing profitability, and maintaining healthy financial ratios. This involves implementing systems to track inventory levels, forecast demand, and optimize ordering processes.

Inventory Turnover and its Impact: Inventory turnover, which measures how efficiently a company sells its inventory, is a key performance indicator reflected indirectly on the balance sheet through the level of inventory held. A high inventory turnover generally indicates efficient inventory management.

Inventory Management and Current Ratio: Efficient inventory management positively impacts the current ratio (current assets/current liabilities). A well-managed inventory level contributes to higher current assets and a stronger current ratio, signifying better short-term liquidity.

Inventory and Business Performance

Inventory levels serve as a strong indicator of a business’s overall health and performance. High inventory levels may suggest overstocking, potential obsolescence, or weak sales, while low levels might indicate supply chain issues or unmet demand.

Industries with Significant Inventory: Industries like retail, manufacturing, and wholesale heavily rely on inventory management and reporting. Accurate inventory accounting is crucial for their financial health and operational efficiency.

Inventory Write-Downs: Inventory write-downs occur when the market value of inventory falls below its carrying cost. This impacts both the balance sheet (reducing asset value) and the income statement (reducing net income).

- Determine the net realizable value (NRV) of the inventory.

- Compare the NRV to the inventory’s carrying amount.

- Record the difference as a loss on the income statement.

- Reduce the inventory value on the balance sheet to reflect the NRV.

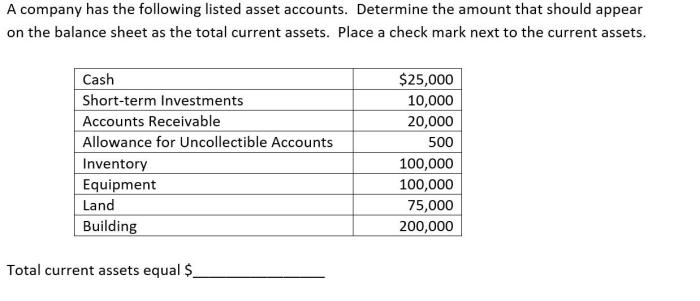

Illustrative Examples of Inventory on Balance Sheets

Source: cheggcdn.com

The following are fictional examples illustrating how different inventory levels and valuation methods affect a company’s balance sheet. Remember, these are simplified illustrations for educational purposes.

Company A: High inventory levels using FIFO. This might indicate overstocking, potentially leading to obsolescence and write-downs. The current ratio might be artificially inflated.

Company B: Low inventory levels using LIFO. This could suggest efficient inventory management, but also the risk of stockouts and lost sales. The current ratio might be lower than Company A’s.

Company C: Moderate inventory levels using weighted-average cost. This might represent a balanced approach, avoiding the extremes of overstocking and stockouts. The current ratio might fall somewhere between Company A and B’s.

A balance sheet’s inventory section typically includes details such as the total inventory value, a breakdown by category (raw materials, WIP, finished goods), and the valuation method used. Obsolescence significantly impacts the balance sheet, leading to write-downs and a reduction in reported asset value. The impact on the income statement is reflected through increased cost of goods sold and decreased net income.

FAQ Compilation

What happens if a company overstates its inventory?

Overstating inventory inflates assets and net income, potentially misleading investors and creditors. It also misrepresents the true cost of goods sold.

How does inventory obsolescence impact the balance sheet?

Obsolete inventory leads to a write-down, reducing the asset value and impacting net income. This reflects a loss of value and potential future losses.

Can inventory be negative on a balance sheet?

A negative inventory balance is unusual and typically indicates errors in record-keeping or potential inventory shrinkage exceeding expectations. It requires immediate investigation.

What is the difference between FIFO and LIFO inventory methods?

FIFO (First-In, First-Out) assumes the oldest inventory is sold first, while LIFO (Last-In, First-Out) assumes the newest inventory is sold first. These methods impact cost of goods sold and net income differently, particularly during periods of inflation.